Let's find your dream home

Featured Properties

Check out my featured properties.

New - 223 Hours

Open House

Virtual Tour

Price Increase

(1d)

4 bd

4 ba

3364 CARMELO Avenue, Coquitlam, BC V3B0E8

Listing Courtesy Of: Keller Williams Ocean Realty

New - 536 Hours

Open House

Virtual Tour

46018 BONNY Avenue, Chilliwack, BC V2P3H6

Listing Courtesy Of: Keller Williams Ocean Realty

New - 1 Hour

Open House

Virtual Tour

4 bd

3 ba

3716 ULSTER, Port Coquitlam, BC V3B7H1

Listing Courtesy Of: Sutton Group - 1st West Realty

New - 2 Hours

Open House

Virtual Tour

1 bd

1 ba

13438 CENTRAL #703, Surrey, BC V3T0N2

Listing Courtesy Of: Laboutique Realty

New - 2 Hours

Open House

Virtual Tour

2 bd

2 ba

9143 154 #910, Surrey, BC V3R9G8

Listing Courtesy Of: eXp Realty (Branch)

New - 3 Hours

Open House

Virtual Tour

5 bd

4 ba

2678 KLASSEN, Port Coquitlam, BC V3C5Y8

Listing Courtesy Of: Oakwyn Realty Ltd.

New - 3 Hours

Open House

Virtual Tour

1 bd

660 NOOTKA #906, Port Moody, BC V3H0B7

Listing Courtesy Of: Rennie & Associates Realty Ltd.

New - 3 Hours

Open House

Virtual Tour

3 bd

3 ba

19452 FRASER #45, Pitt Meadows, BC V3Y0A3

New - 3 Hours

Open House

Virtual Tour

4 bd

3 ba

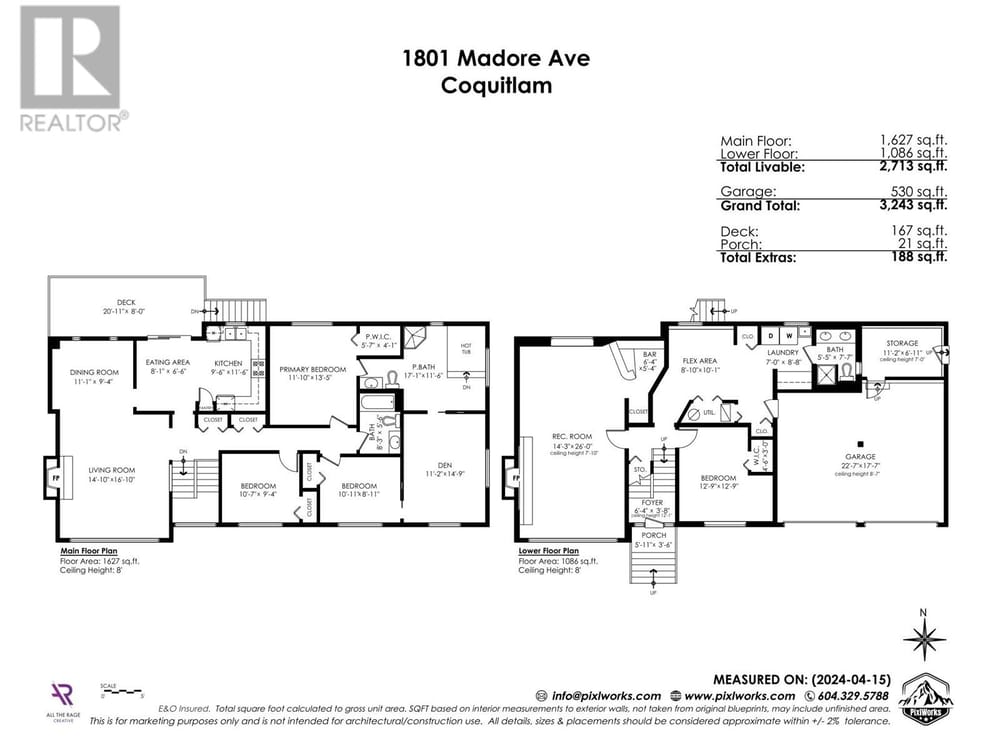

1801 MADORE, Coquitlam, BC V3K5R1

Listing Courtesy Of: RE/MAX Treeland Realty

New - 3 Hours

Open House

Virtual Tour

1 ba

531 COCHRANE, Coquitlam, BC V3J2A1

Listing Courtesy Of: Angell, Hasman & Associates Realty Ltd.

Featured Testimonials

My Blog (Buyers Guide)

Explore our blog posts to learn from the best about buying selling and maintaining your home

Housing Affordability will always be an issue, Governments need to help and not escalate costs.

Taxes, Filings related to Real Estate in British Columbia and Canada

Aman Brah

License #: 142449

Keller Williams Realty | Aman Brah Real Estate Marketing

Mobile

Office

Contact Me